Microeconomics (small economics) is about the decision-making behavior of individuals and firms regarding how to allocate scarce resources and their interactions.

Production Possibility Frontier (PPF)

The “Production Possibility Frontier (PPF)“ represents the maximum output that an economy can produce at any given moment. (often illustrated as a “Guns & Butter” trade-off)

- PPF is a boundary that separates the attainable from the unattainable.

- If the production of goods occurs at the point on the PPF curve, the economy is productively efficient because it uses all available resources.

- At the productively efficient point, we face a trade-off.

- The economy can produce only one more product by producing another less. (opportunity cost)

- Producing at the point INSIDE the PPF signifies productive inefficiency, indicating unused or misallocated resources.

- However, with international trade, the consumption can be outside of the PPF.

Opportunity Cost

- Resources have alternative uses.

- The opportunity cost is the highest-valued alternative forgone.

Demand

- A demand curve represents the relationship between the demand (as the quantity of goods) and price.

- The typical shape of the demand curve is downward-sloping: lower demand at higher prices.

- The Movement along the demand curve:

- The price change leads to a change in demand.

- The shift of a demand curve:

- Outward, right shift: more demand at the same price

- Inward, left shift: less demand at the same price

- Reasons for shifts

- A change in income

- normal or superior goods: right-shift

- inferior goods: left-shift

- Marketing

- A change in the number of buyers

- A change in the price of substitute/complement products

- A change in social patterns

- A change in income

The Law of Diminishing Marginal Utility

- As a buyer consumes an additional unit of a product, the additional utility (satisfaction) will decline.

Elasticity of Demand

Price Elasticity of Demand = (% change in demand) ⁄ (% change in price)

- Inelastic ( < 1 ): not price sensitive

- Unitary elastic ( =1 ): proportional

- Elastic ( > 1 ) : sensitive

- Total Revenue (TR) is an earning: TR = Price per unit × quantity sold

- If the demand is elastic, an increase in price will lead to a fall in revenue.

Income Elasticity of Demand = (% change in demand) ⁄ (% change in income)

Cross Price Elasticity of Demand = (% change in demand (product A)) ⁄ % (change in price (product B))

The following table shows how the different types of elasticity work:

| Elasticity of Demand | Direction of Demand | Size | Type of Product |

| Price (+) | (-) : Elastic | > 1 | |

| Price (+) | (-): Inelastic | < 1 | |

| Price (+) | (+) | Veblen goods or Giffen goods | |

| Income (+) | (-) | Inferior | |

| Income (+) | (+): Elastic | > 1 | Luxury |

| Income (+) | (+): Inelastic | < 1 | Necessity |

| Cross (+) | (-) | Substitutes | |

| Cross (+) | (+) | Complements |

- Veblen goods and Giffen goods violate the basic law of demand: consumers purchase more when the price increases.

- Veblen goods: A price change modifies the consumer’s perception of the good. It might be of its exclusive nature or an appeal as a status symbol.

- Giffen goods: A non-luxury product that lacks close substitute goods. Examples can include bread, rice, and wheat.

Supply

- Supply is the amount producers are willing to produce at each price.

- The supply curve is generally upward-sloping; more supply at a higher price.

- The shift of a supply curve

- Inward, left shift: less supply at the same price

- Outward, right shift: more supply at the same price

- Reasons for shifts

- A change in the number of producers

- A change in technology

- A change in cost

- A change in taxes

Price Elasticity of Supply = (% change in supply) ⁄ (% change in price)

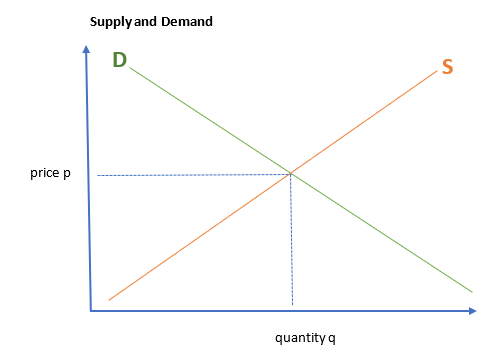

Supply and Demand: Market Equilibrium

- Market Equilibrium is the point where the demand and the supply are equal.