The basic concepts of Costs, Revenues, and Profits.

The following cover the basic concepts in the mainstream (Capitalist, neo-classical) Economics.

Costs

Total Costs (TC) = Fixed Costs (FC) + Variable Costs (VC)

The Law of Diminishing Returns

Marginal Product (MP) = (change in total output) ⁄ (change in the variable factor)

- Productivity will be reduced whenever the additional variable factor is added.

Marginal Costs

Marginal Costs (MC) = (Change in TC) ⁄ (Change in output)

- Marginal cost (MC) is the inverse of MP (Marginal Product).

- MC is the extra cost incurred when one extra unit of output is produced.

- Each additional factor leads to a higher cost -> Diminishing Return

Average Costs (AC)

TC = FC + VC

AC = TC ⁄ Q = FC ⁄ Q + AC ⁄ Q = Average Fixed Costs (AFC) + Average Variable Costs (AVC)

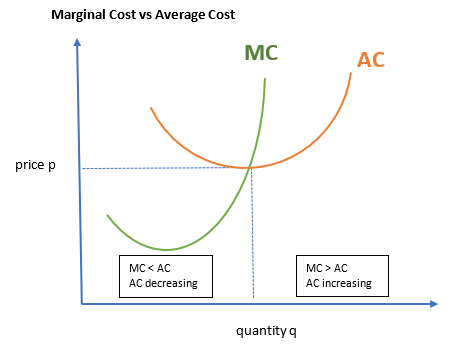

Marginal Costs (MC) vs. Average Costs (AC)

- MC > AC: pull AC up

- MC < AC: bring AC down

- MC will cross AC at the AC’s minimum point

Long-run Costs

- Economies of Scale

- The company can reduce the Average Costs (AC) when it produces more.

- Diseconomies of Scale

- If the company grows too large, it may find the AC begin to rise again.

- Minimum Efficient Scale (MES)

- The first point of output at which the long-run AC is minimal.

Revenues

Total Revenue (TR) is the measurement of sales.

Total Revenue (TR) = Price (P) × Quantity (Q)

Marginal Revenue (MR) is the difference in Total Revenue when an additional unit is sold

Marginal Revenue (MR) = (change in TR) ⁄ (change in Quantity)

Profits

Profit = Total Revenue (TR) – Total Costs (TC)

Profit Maximization

A company should stop producing at the point where Marginal Revenue (MR) equals Marginal Costs (MC)

- MR > MC: extra unit will make a profit

- MR = MC: no extra profit

- MR < MC: extra unit will be a loss